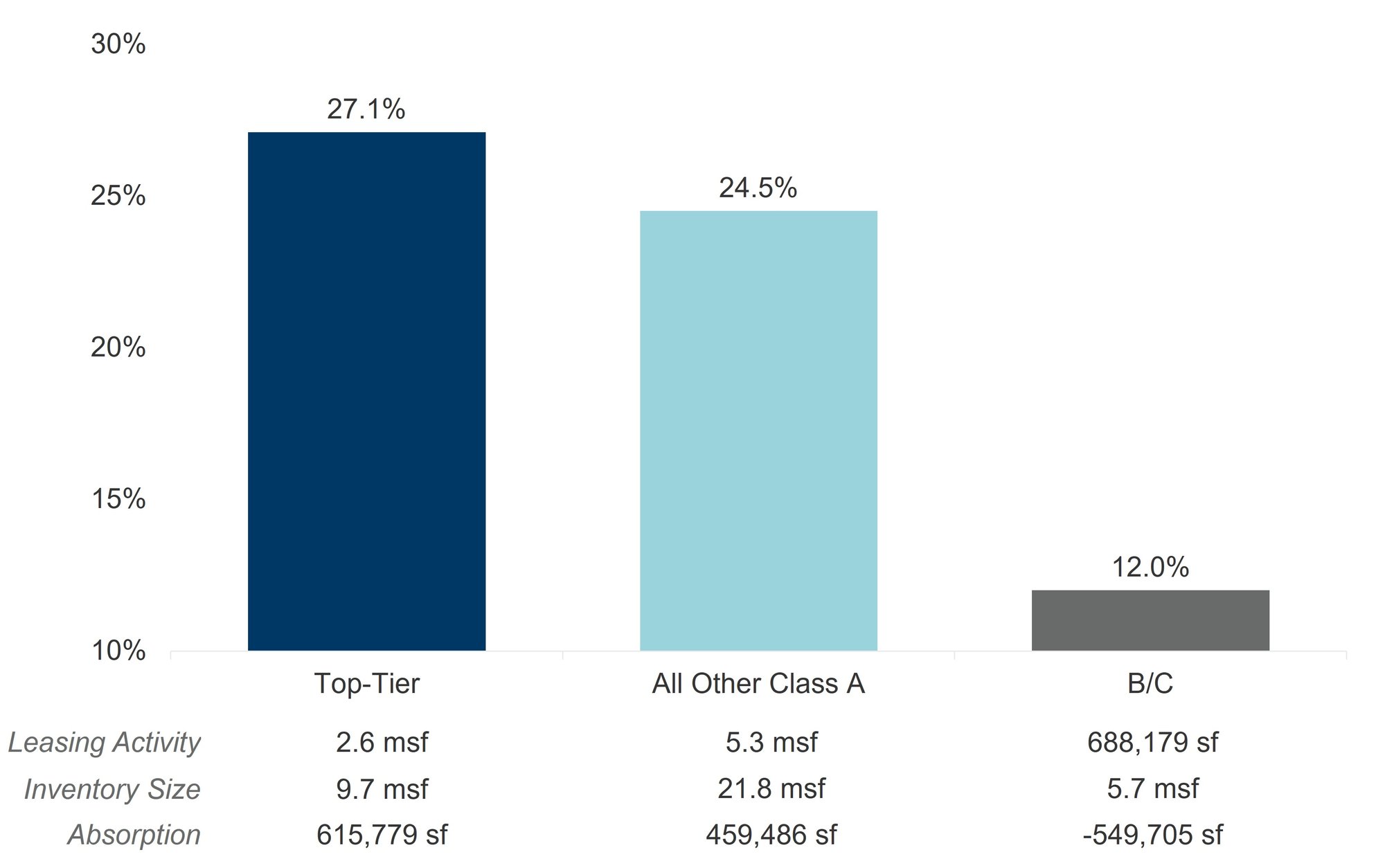

Downtown Dallas’ set of top-tier properties lead all other categories of CBD (Central Business District) office product in terms of leasing, absorption and rental rates. It is important to note the differences in the total inventory tracked in the CBD. Of the total 27.8 million square feet (msf) tracked, top-tier properties make up 34.8% of inventory, while non-top-tier Class A account for 44.6% of CBD inventory. Top-tier properties recorded a total of 2.6 msf of leasing activity from 2020 to present day, which is 27.1% of the total top-tier inventory, and a current gross rental rate of $36.59 per square foot (psf). Non-top-tier Class A properties recorded 5.3 msf of leasing activity during the same period, 24.5% of the inventory, and a current gross rate of $32.37 psf. Class B and C office properties recorded the lowest leasing activity totaling 688,179 sf, just 12.0% of its office inventory, and a current gross rate of $22.27 psf. Rental rates for top-tier properties in the CBD commanded a 64.3% premium over Class B and C properties.

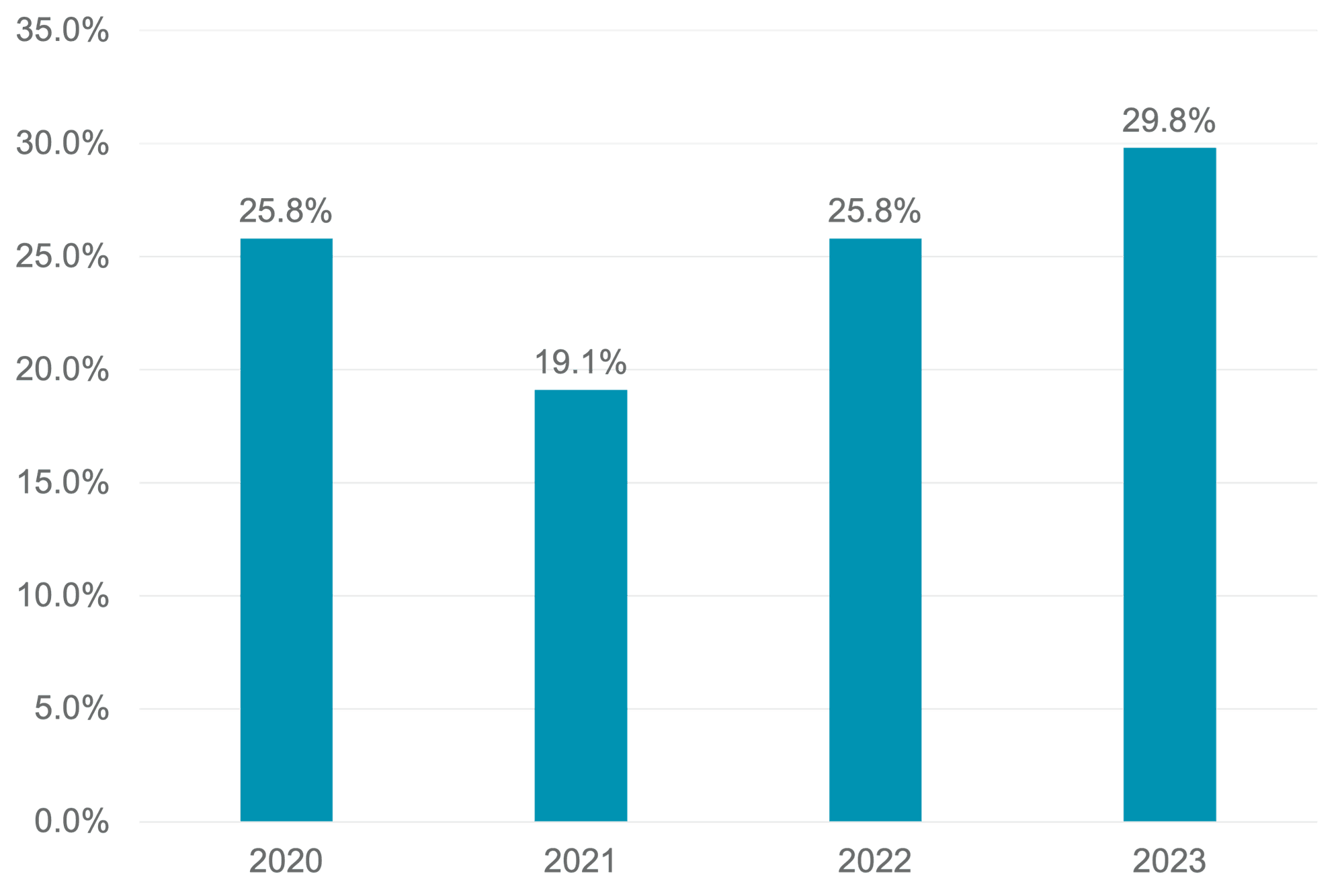

One area of focus in the CBD submarket, along with Dallas as a whole, is the elevated levels of sublease space being brought to market. While the entire DFW market recorded a total of 12.5 msf of available sublease space at the end of Q4 2023, levels which are off their peak of 12.6 msf in Q2 2023, the CBD had just 1.3 msf of available sublease space at the end of Q4 2023.